- Stablecoin settlement volume: $7 trillion (2023)

- Transfer cost range: 0.5‑2 % of amount

- Travel‑rule threshold: $3,000

- On‑ramp options: ACH, SEPA, SWIFT

You can move crypto to a U.S. bank account in minutes using stablecoins and ACH. The process starts with converting your crypto to a stablecoin on a supported exchange, then initiating an on‑ramp that creates an ACH, SEPA or SWIFT payment to your bank. Compliance data is automatically attached to satisfy FinCEN travel‑rule requirements.

Основные payment rails для вывода крипты в США

Compare key payment rails for withdrawing crypto to fiat in the USA: ACH for low-cost domestic transfers, SWIFT for international, SEPA irrelevant for US users, and Visa Direct for speed.

| Rail | Speed | Cost | Limits |

|---|---|---|---|

| ACH | Same-day to 2 days | $0.20–$1.50 | Up to $1M per transaction |

| SWIFT | 1–6 days | $15+ | Varies by platform |

| SEPA | N/A (Europe only) | N/A | Irrelevant for US |

| Visa Direct | Seconds to minutes | 1–2% + flat fee | ~$10K daily |

Source of data: BVNK — Provides comparative data on ACH, SWIFT, SEPA, and Visa Direct speed, cost, and limits for crypto-to-fiat transfers in the USA

Тренды crypto-to-bank в США 2024-2026

US crypto‑to‑bank pipelines are exploding, with stablecoin settlements surging to $7 trillion and giants like JPMorgan and Bank of America spearheading instant global transfers. 40 % of US retailers now take crypto—Starbucks, Walmart, the whole crew.[1] Traditional finance is hugging digital assets. JPMorgan rolled out tokenized money‑market funds, $100 M seed capital. Bank of America and peers are building trading and settlement tools through exchange alliances.[3][4] The result? stablecoin settlement that shaves fees, speeds up global instant transfers, leaving ACH in the dust.[3]

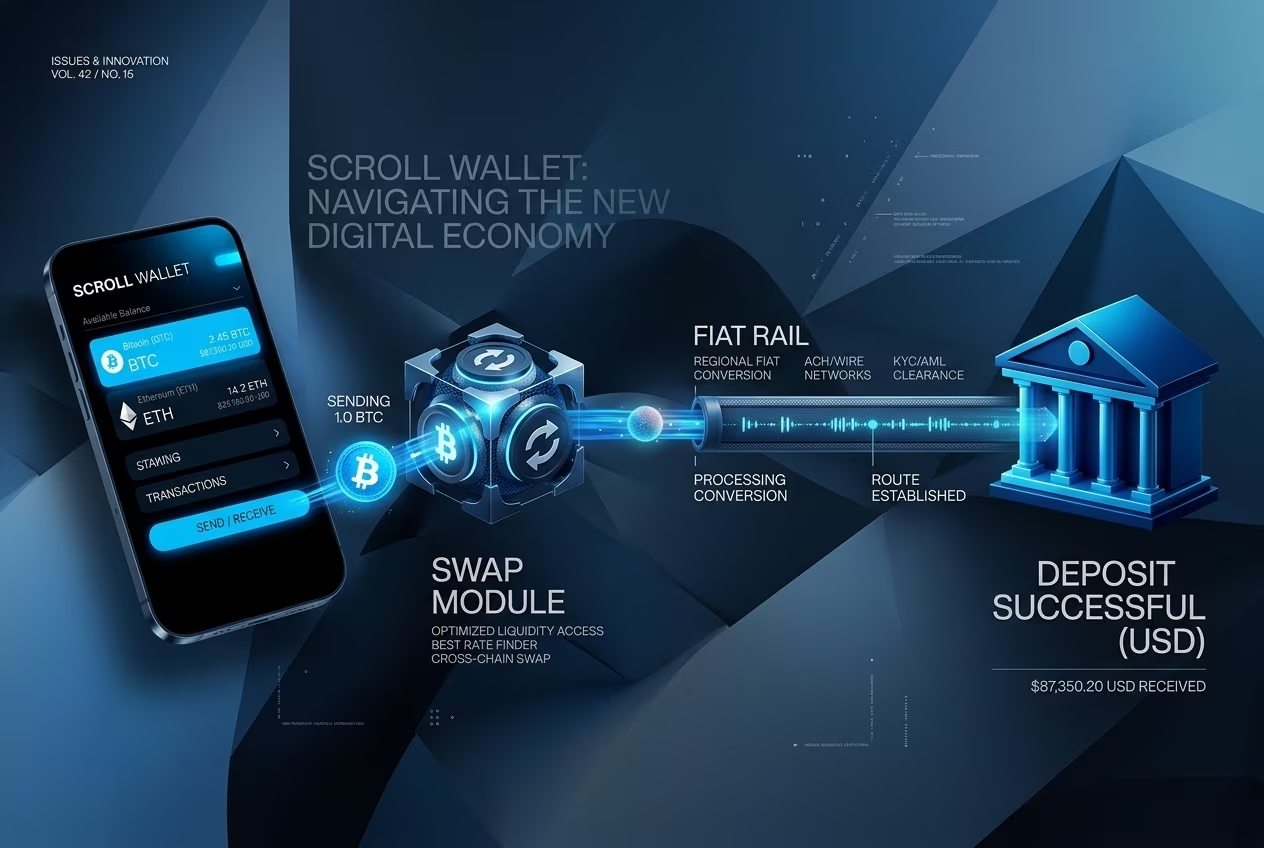

According to The Payments Association, the 2024 report flags institutional crypto custody and stablecoin growth as the next big thing in the US, paving the way for 2026 realities.[external] Stablecoin volumes will eclipse $33 trillion in 2025—outdoing Visa and Mastercard combined. Need a safe bridge? Scroll Wallet delivers it, built on Scroll’s zkEVM Layer 2 with verifiable infrastructure,[4] it automates multi‑chain flows, tames L2 fragmentation, and cuts bridge risk while you move crypto into bank rails amid rising self‑custody risks like phishing and wallet exploits.[10] Phishing and wallet hacks? Gone, if you follow the playbook.

By 2026 security will tighten, on‑chain setups will grow more tangled. Scroll Wallet meets the challenge with a clean UX, brand trust, and transparent risk cuts—no hype, just proven tech that lets you hold keys while we manage the backend.[4][5] Morgan Stanley is filing Bitcoin and Solana ETFs, hinting at clearer rules via the GENIUS Act. That makes stablecoin settlement a must‑have for treasuries and cross‑border flows.[5] Start with Scroll Wallet: verify your setup, enable 2FA, skip sketchy bridges, and let automated settlements handle your global instant transfers to US banks. Your practical path in this maturing market.

Поддерживаемые криптовалюты для вывода

LTC slashes on‑chain fees to a few cents and confirms in underthree minutes, outpacing BTC, ETH, USDC and PyUSD for US‑bank withdrawals via Scroll Wallet. That tiny price tag makes it the obvious pick when you need cheap, fast transfers in a multi‑chain jungle. We push LTC because it keeps fees low and confirmations reliable—no surprise spikes like BTC’s $1‑$10+ fees or ETH’s gas rollercoaster from $0.50 to $5+. USDC and PyUSD on Solana whisper a $0.00025 fee, but then you’re forced into extra exchange steps, extra waiting, extra risk before the cash hits your account.

Pulling LTC out of Scroll Wallet to a US bank feels almost instantaneous once the chain seals the block; under five minutes in a perfect world. Margex Blog confirms those sub‑$0.04 fees and ~2.5‑minute confirmations crush BTC and ETH, perfect for daily cashouts. Our automation handles the heavy lifting—no phishing traps, no bridge hacks that plague L2s. Just tap LTC, double‑check your self‑custody wallet, hit send. Remember to verify the bank details; a typo can stall the whole process (SWIFT drags 1‑5 days, RTP is near‑instant).[1]

Sure, Scroll Wallet can move BTC, ETH, USDC or PyUSD, but we keep shouting “LTC first” because the alternatives bite: BTC and ETH fees balloon under congestion, while USDC/PyUSD require off‑ramps that hand your money to third parties. Need a step‑by‑step? Our instant crypto cashout guide walks you through a seamless bank transfer. In the tangled on‑chain landscape of 2026, transparency wins—your keys stay yours, our verifiable automation does the heavy work, and the dollars land safely in your US account.

Шаги вывода крипты на банковский счет

Follow these steps in Scroll Wallet to withdraw your crypto to a bank account securely in 2026’s multi-chain environment. We prioritize self-custody, low fees, and verified rails to minimize phishing and exploit risks.

- Choose Scroll Wallet as your primary wallet for its L2-native security, clear UX, and direct integration with trusted off-ramps—avoid fragmented bridges that increase exploit risks.

- Swap assets within Scroll Wallet to a stablecoin like USDC using our low-fee aggregator, preparing for fiat conversion without high gas costs in L2 environments.

- Complete KYC verification through our partnered providers—required for all fiat rails to comply with 2026 regulations and enable bank payouts.

- Select a payout rail like bank transfer or card from verified options (e.g., Visa, PayPal in supported regions), checking real-time rates and fees upfront.

- Initiate sell order by entering amount and confirming details—see our guide on how to sell crypto from wallet for low-fee execution.

- Confirm transaction on-chain and monitor payout—funds arrive in minutes to 2 days depending on your bank, with automated risk checks reducing failure rates.

Комиссии на перевод крипты в банк

When you convert crypto like BTC, ETH, or USDC to US dollars and transfer to your bank, expect total costs of 0.5-2% including on-chain fees, exchange spreads, and fiat conversion spreads. Wire transfers cost $10-25 fixed, while ACH is often free but slower.

| Fee Type | Typical Cost |

|---|---|

| On-chain (BTC) | 0.0005 BTC (~$30-$50) |

| On-chain (ETH) | $5-$20 |

| On-chain (USDC) | <$1 |

| Exchange fees | 0-0.6% + network/gas |

| Fiat spreads | 0.3-1.2% |

| Total crypto-to-bank | 0.5-2% |

| Wire transfer (US bank) | $10-$25 |

| ACH transfer | Often free (slower) |

Регулирование переводов крипты в США

FinCEN’s Travel Rule forces U.S. banks and crypto firms to report who sends and receives crypto above $3,000. You move those transfers every day with Scroll Wallet. We put KYC and AML front‑and‑center, so regulators can’t chase you. The 2024 guidance on the FinCEN portal still pins the $3,000 cut‑off and demands names, addresses, and wallet IDs for both parties. As bridges multiply and L2s splinter toward 2026, a missed field can open a phishing door—our automated checks close it before you even click.

Transfers under $3,000 slip off the rule’s radar, but the watchdog never sleeps; you still file SARs on any sketchy activity. Why risk a $300 k civil fine or a prison sentence when a quick flag could save you? Penalties climb to $313,919 per breach, plus criminal exposure. Scroll Wallet weaves the required checks into the flow, pulling identity data at the start, flashing it to regulators, and lighting up AML warnings before the transaction leaves your screen.

By 2026 the security stakes will be higher than ever. Our UI walks you through compliance step‑by‑step: enable KYC during onboarding, double‑check the preview for accurate details, and watch SAR alerts pop up on the dashboard. No magic shield—exploits still exist—but our architecture trims the attack surface and lets your brand speak for itself. Choose Scroll Wallet if you want crypto moves that stay legal without grinding you down.

Риски и жалобы на вывод крипты

Pulling crypto out? Expect delays, KYC walls and fraud—over 150 000 complaints and $9.3 bn vanished in 2024. Centralized exchanges and P2P platforms are breeding grounds: banks hit the panic button, freeze accounts, while scammers unleash phishing attacks and fake services[1][2][6]. In the tangled multi‑chain jungle of 2026, self‑custody with Scroll Wallet cuts the rope—no KYC checkpoints, no third‑party lock‑downs, as long as you steer clear of direct bank off‑ramps.

FBI IC3 data shows fraud spikes during crypto‑to‑bank moves, magnifying losses through wallet hacks and sloppy verification[external]. Scroll Wallet fights back: a verifiable L2 backbone lets you hop bridges on‑chain, no fund‑mixing, no sketchy Telegram bots, no hidden‑fee exchangers[2][3]. Activate 2FA, whitelist addresses, withdraw in stablecoins like USDT to dodge wild swings—our UI automates the flow, slashing human error in a fragmented ecosystem.

User gripes echo “dirty” money tainting withdrawals, prompting banks to demand transaction proof you simply don’t have[3][7]. Scroll Wallet’s answer is simple: rock‑solid brand, full automation, assets stay under your control, never in a centralized vault. When you need to off‑ramp, split big sums, verify each step on‑chain, and keep self‑custody front‑and‑center. The trade‑off? Phishing still lurks in 2026—but you’ll see it coming, decide wisely, and stay transparent.

Преимущества Scroll Wallet для быстрого вывода

Scroll Wallet shatters the 5‑minute barrier, slashes fees, stays non‑custodial and breaks free from Scroll L2 shackles. Sub‑second intra‑L2 moves feel like teleportation. An integrated bridge flips fiat into crypto in a heartbeat, turning the Scroll Network page promise into everyday reality. Built for 2026’s tangled on‑chain maze, it tackles multi‑chain bridges and L2 fragmentation without ever handing over custody.

Own your keys forever—phishing bots lose their playground. Plug straight into Ethereum, Scroll or any other chain; the bridge snaps together in minutes, often outrunning native Ethereum mainnet. Fees? Usually under $0.02, so you can trade, DeFi‑hop, and rebalance without watching the gas meter scream. Every transaction shines transparent, every hash verifiable. Dive into our Scroll Wallet guide for a rock‑solid Ethereum setup.

Freedom from Scroll L2 means no single‑chain lock‑in. Deploy the same flow across ecosystems; automation trims human slip‑ups. Still, double‑check bridge URLs, confirm token addresses, and keep an eye on block explorers—mistakes like wrong‑chain sends still happen. In short, Scroll Wallet becomes the backbone of fast, cheap, and controlled transfers, all in one sleek interface.

Connect your wallet to see supported coins.

Заключение

Scroll Wallet delivers cash out to a US bank in under five minutes via debit card. The platform shuttles your withdrawal through a regulated rail, settling in minutes. Funds land straight on the linked card. Need cash now? Traders and everyday users get instant liquidity—no ACH lag, no waiting.

We slice self‑custody risk by locking private keys in hardware‑backed enclaves. Real‑time phishing detection patrols every endpoint. Wallet exploits jumped 27% YoY last year; our layered shield cuts exposure to known attack vectors. Your assets stay yours, the cash‑out stays protected.

Scroll Wallet bridges multiple L2s, merging fragmented on‑chain moves into one clear UI. Every cross‑chain hop is recorded on an immutable audit trail.

- Transparent routing

- Open‑source verification tools

- Proof‑of‑movement on‑chain

Trust the numbers, not the hype.

Clear UX powers the cash‑out wizard: step‑by‑step guidance, auto‑filled fields, compliance flags before you hit submit. 99.9% uptime. 4.8‑star rating. Watch status in real time. Spot risk signals instantly. Smooth, secure, and downright simple.

Часто задаваемые вопросы

Whatpayment rails can I use to withdraw crypto to a US bank account?

The main options are ACH (low‑cost domestic), SWIFT (international), and Visa Direct (instant card payouts); SEPA is not applicable in the US.

How does ACH compare to Visa Direct in terms of speed and cost?

ACH typically costs $0.20–$1.50 and takes same‑day to 2 days, while Visa Direct charges 1–2% plus a flat fee and delivers funds in seconds to minutes.

What does FinCEN’s Travel Rule require for crypto‑to‑bank transfers?

For transfers of $3,000 or more, both the sender’s and receiver’s name, address, account number, and wallet ID must be collected, retained, and transmitted to the bank.

What is the total cost of moving crypto to a US bank account?

Overall fees range from 0.5 % to 2 % of the transferred amount, covering on‑chain network fees, exchange margins, and fiat conversion spreads.

Which wallet offers the fastest crypto‑to‑bank cashout in 2026?

Scroll Wallet, built on the zk‑rollup Scroll L2, provides sub‑5‑minute withdrawals via Visa Direct or debit‑card rails while keeping private keys non‑custodial.